To pursue the fulfillment of rights relating to payment, one shall first understand the types of mechanism available at law. Under the civil law regime in Indonesia, non-performance of payment obligation may be pursued through, among others, civil lawsuit (gugatan perdata) mechanism based on the general civil law framework or suspension of debt payment obligation petition (Permohonan Penundaan Kewajiban Pembayaran Utang / PKPU). In the event of payment obligation non-performance, choosing a correct legal strategy would be crucial as it determines how the court would grant an order to fulfill the obligation in question. To choose the correct mechanism, one shall understand the nature of the evidence and goal.

Civil Lawsuit

Under Indonesia’s general civil law regime, civil lawsuit has been used as the most common mechanism in the event of payment non-performance. However, civil lawsuits do not only revolve around payment non-performance. It is in principle applicable to all forms of contractual obligation non-performance. Therefore, the main requirement of submitting a civil lawsuit would be the existence of a valid agreement, the element of which pursuant to Article 1320 of the Indonesian Civil Code consists of consent, capacity, the existence of a subject-matter, and lawful cause.

It is to note, however, a valid agreement would not be the only element one shall take into account in taking civil lawsuit mechanisms. According to Article 1238 of the Indonesian Civil Code, a party is deemed in default either by an order or a deed of the like, or pursuant to the agreement itself (e.g. the agreement sets out that the party shall be in default upon failure to perform within the agreed time period). Therefore, in taking civil lawsuit mechanisms, the defaulted parties are initially required to deem the other party as being in default of the agreement in question, either by an existing contractual clause or a letter as commonly known as a “cease and desist” / demand letter (somasi).

In general, civil lawsuits are taken in cases where disputes are complex. Though there is no formal interpretation as to the requirement of a dispute being complex, the parameter of determining whether a dispute is likely to be deemed complex is implied under Article 2 paragraph (1) of Law Number 37 of 2004 on Bankruptcy and Suspension of Debt Payment Obligation (“Bankruptcy Law”). Under the said provision, it is stated that a case may only be brought to court for bankruptcy petition if the debtor has 2 (two) or more creditors and a debt that is due and payable. Therefore, a case may be deemed complex if it does not fulfill the said elements. An example of a complex case would be if there is a dispute over the existence of a debt, complicated debt calculations, dispute over due dates, complex legal relationships, and so forth.

When taking civil lawsuit mechanisms, the defaulted party must be aware that pursuant to Article 1243 to Article 1251 of the Indonesian Civil Code, remedies may consist of costs, damages, and interests (CDI), either materially or immaterially, with note that such CDI is not payable in uncontrollable and/or unforeseeable events (force majeure).

On the downside, civil lawsuits often require a relatively long time to take effect, as the judgment of the courts of the first instance is not final and binding. Therefore, the opposing party may file for an appeal through the high courts, the judgment of which would also not be final and binding. This leads to the possibility of the party in question filing for a cassation through the Supreme Court. Normatively, judgments rendered by the Supreme Court are final and binding. However, any party may file for a judicial review (peninjauan kembali) for cases where new material evidence and/or circumstance are discovered after the judgment was rendered but has existed before the judgment was rendered. Subsequent to the courts rendering a final and binding judgment, if the debtor still refuses to pay, the creditor must then apply a petition for execution to the head of the local district court, and the process entails a warning (aanmaning), executory seizure, and a public auction.

PKPU Petition

While a civil lawsuit focuses on establishing a breach of contract and awarding damages, a PKPU petition serves as a specialized collective legal mechanism designed for debt recovery and corporate resuscitation. Under the Bankruptcy Law, PKPU is often favored by creditors seeking a faster and higher-pressure route to settlement.

The core idea or philosophy of PKPU is not the immediate liquidation of the assets of the debtor, but rather a legal moratorium to facilitate debt restructuring. Under the supervision of the Commercial Court, PKPU provides a respite for debtors who are unable or debtors who foresee that they will be unable to continue paying their debts. The objective is to reach a composition plan (rencana perdamaian) between the debtor and the creditors, which may often include rescheduling payments or debt-to-equity swaps, thereby ensuring the debtor’s business continuity while maximizing debt recovery for the creditors.

To initiate a PKPU petition, a creditor must satisfy the strict cumulative requirements as set out under Article 222 paragraph (1) of the Bankruptcy Law. The requirements of which mirror those of bankruptcy, requiring that debtor to have two or more creditors and at least one due and payable debt. Unlike a civil lawsuit, a PKPU petition does not require a prior “cease and desist” letter (somasi) to be legally valid, though it remains a common practice to demonstrate the debtor’s inability to pay.

The most critical procedural filter for a PKPU petition is the principle of summary evidence (pembuktian sederhana), as set forth under Article 8 paragraph (4) and Article 224 of the Bankruptcy Law. This means that the court will only grant a PKPU petition if the facts or circumstances concerning the existence of the debt and the requirements in Article 222 paragraph (1) can be proven simply.

If the Commercial Court finds that the debt calculation is complex, the legal relationship is disputed (e.g. a challenge to the validity of the underlying contract), or the case requires extensive witness testimony, the petition must be rejected. In such instances, the court will direct the parties to resolve the dispute via a general civil lawsuit. This nature is what allows PKPU proceedings to be significantly faster than civil litigation.

As debtors may also file for PKPU, debtors must be aware that this mechanism may cause severe consequences if an agreement is not reached. For instance, pursuant to Article 230 of the Bankruptcy Law, in the event that the creditors do not approve the composition plan or the court refuses to ratify an approved composition plan (homologasi), the court must promptly declare the debtor in question bankrupt (pailit).

Once bankruptcy is declared, the debtor effectively loses all rights to manage its assets. The assets will then be placed under the control of a receiver (kurator) for liquidation. This inherent risk creates a powerful incentive for debtors to negotiate seriously and offer favorable settlement terms during the PKPU process.

Strategic Risks and Pitfall

Unlike bankruptcy, where a receiver takes full control of the debtor’s assets, the PKPU regime operates on the principle of “debtor in possession”. Pursuant to Article 240 of the Bankruptcy Law, the debtor remains entitled to manage its assets and business, provided that such action must be conducted jointly with the court-appointed administrator (pengurus). For a creditor, the risk lies in the debtor’s potential to mismanage the business or diminish asset value during the proceedings. While the administrator acts as a supervisor, the creditor does not have the same level of direct control over the collateral as they might have during an execution process in a civil lawsuit.

On the other hand, the most common pitfall for creditors in PKPU is the “simple evidence” requirement as set forth under Article 8 paragraph (4) of the Bankruptcy Law. If the debt arises from a complex contract (e.g. construction contract with liquidated damages, derivative transaction, contracts where the fulfillment of the condition precedent is disputed), the Commercial Court will reject the petition, ruling that such cases belong in a District Court civil lawsuit due to the fact that the debt is not “liquid” or easily/simply verifiable. If the court determines that it must examine deep contractual intent or verify extensive technical aspects to establish the debt’s existence, the PKPU petition will be dismissed and the creditors have to start over in the District Court with civil lawsuit, not to mention the spent significant time and legal fees.

Key Decision Factors

The most compelling reason to choose PKPU over civil lawsuits is speed. A civil lawsuit is subject to the standard judicial hierarchy, where a final and binding nature of the judgment can take years to achieve. Conversely, under Article 228 paragraph (6) of the Bankruptcy Law, the total duration of a PKPU cannot exceed 270 days. If no agreement is reached within the said timeframe, the debtor is automatically declared bankrupt.

As regards to costs, a civil lawsuit generally involves lower upfront costs which primarily consist of court filing fees. However, PKPU involves significant professional costs. In a PKPU, the petitioner may be responsible for the administrator’s fee, which is often calculated based on a percentage of the total debt. Though being more expensive, the high cost of PKPU is often perceived as an investment in a significantly faster recovery.

Additionally, the outcome of a successful PKPU is a ratified composition plan (rencana perdamaian yang dihomologasi). Under Article 286 of the Bankruptcy Law, a ratified composition plan legally binds all creditors, even those who voted against it. In contrast, a civil lawsuit ends in a judgment. While a judgment is powerful, it often requires a separate execution process, not to mention that if the debtor remains uncooperative. A PKPU ratified composition plan avoids this by forcing the debtor to the negotiating table under the immediate threat of liquidation.

Conclusion: When to Choose Which?

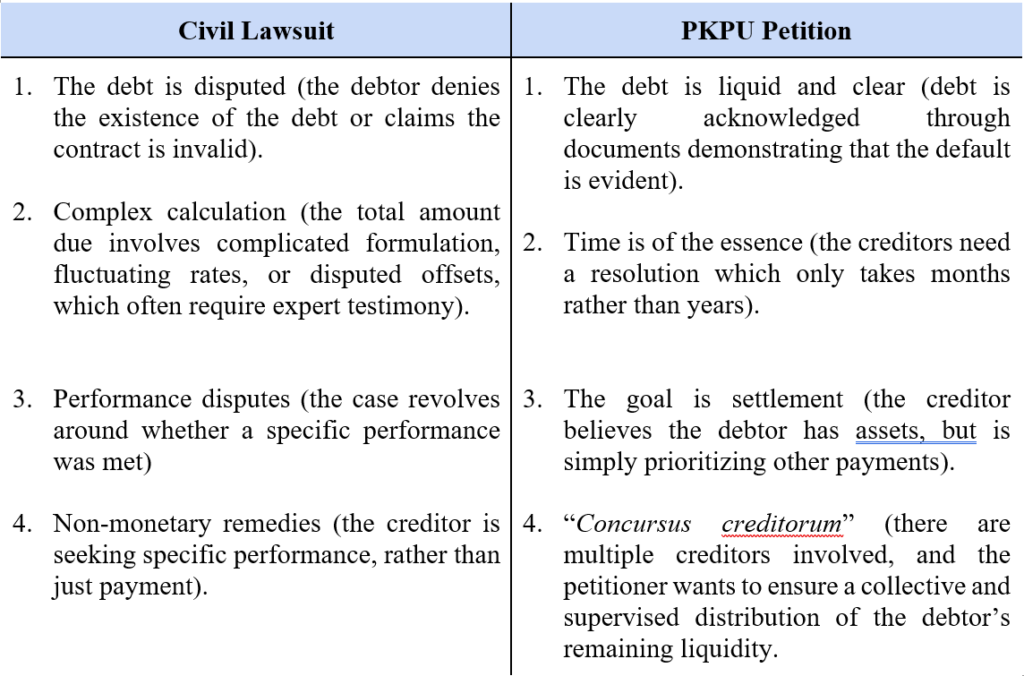

Deciding between a civil lawsuit and a PKPU petition is a high-stakes tactical choice that depends entirely on the nature of the evidence and the creditor’s ultimate objective. While the PKPU mechanism offers a powerful “express” route to recovery through the threat of insolvency, its strict evidentiary requirements make it a risky choice for disputed or poorly documented claims. In contrast, a civil lawsuit provides the necessary depth for complex legal arguments, but requires the patience to navigate a multi-year judicial process. The following is the summary table of when to choose which strategy:

If you, a prospective client, have further inquiries about the topic discussed above, Schinder Law Firm is one of many corporate law firms in Indonesia that has handled numerous similar matters, with many experienced and professional corporate and civil lawyers in its arsenal, making it one of the top consulting firms in Indonesia. Feel free to contact us at info@schinderlawfirm.com for further consultation.

Author:

Dewi Susanti